Radical Simplicity

We believe that lifetime investment returns are primarily, if not entirely, governed by two variables: asset allocation and behavior. In “Asset Allocation Made Easy,” we outline a simple methodology that explains how to determine the optimal allocation among cash, bonds and equities. The next step is security selection. Here we focus on what equities to buy and why.

What equities to buy?

When it comes to building a fully diversified equity portfolio, an investor merely needs to own two broad-based equity index funds. We recommend buying one domestic equity index fund and one international index fund, usually allocating 80% of investments to the former and 20% to the latter.[1] That’s it.

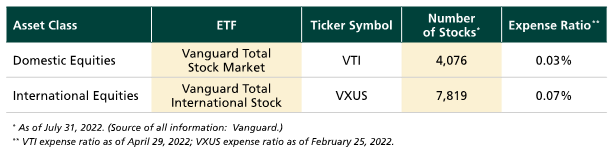

To understand why this strategy works, consider the two Vanguard exchange-traded funds shown in the table below. Based on their holdings as of July 31, 2022, an investor in these funds would own shares in 11,895 of the leading companies in the world—effectively the entire global stock market—on a market capitalization-weighted basis.

For practical purposes, fund expenses are near zero, and tracking error relative to the underlying benchmarks is effectively zero. Since inception in May 2001, and through July 2022, VTI’s annual return (based on price) has trailed its benchmark[2] by just 2 basis points. Since inception in January 2011, VXUS’s annual return has exceeded its benchmark[3] by 3 basis points.

The power of compounding vs. active management

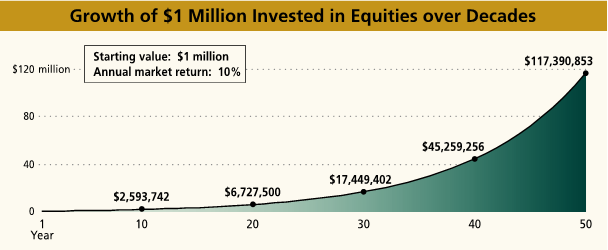

While a small number of active managers have managed to outperform the market over the long term, it’s totally unnecessary to beat the market to enjoy the premium returns of equities. That’s because compounding of average market returns over the long term provides remarkable, sustained growth. Or, as Morgan Housel noted, “The most important investing question is not, ‘What are the highest returns I can earn?’ It’s, ‘What are the best returns I can sustain for the longest period of time?’”[4] The following graph demonstrates the power of compounding average market returns over several decades.

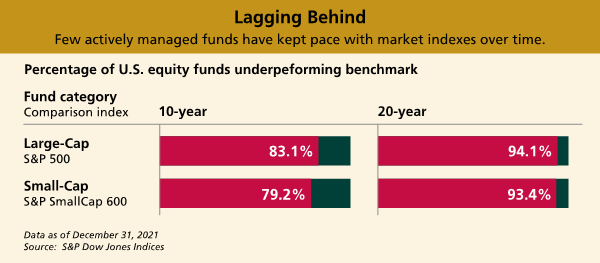

By contrast, active management rarely, if ever, matches this level of equity index returns over the long term. S&P Indices versus Active (SPIVA) scorecards are semiannual reports published by S&P Dow Jones Indices that compare the performance of active equity and fixed income mutual funds against their benchmarks over different time horizons.

Based on the SPIVA U.S. Scorecard for 2021, over the 10-year period ending December 31, 2021, 83.1% of U.S. large-cap funds underperformed the S&P 500, while 79.2% of small cap-funds underperformed the S&P SmallCap 600 index. For the 20-year period, the percentage of large-cap and small-cap funds underperforming their benchmarks were 94.1% and 93.4%, respectively.

In his folksy way, Vanguard founder Jack Bogle explains why passive funds do better: “In the fund business, you get what you don’t pay for.” Manager fees, trading costs, and taxes erode the returns of active managers. By contrast, these expenses are near zero for passively managed equity index funds.

Complete equity portfolio with just two funds

Thanks to the virtues of equity index funds, which are broadly diversified, low-cost and tax-efficient, it takes only two funds to form a complete equity portfolio. That’s radical simplicity.