There Is No Alternative

2019 wasn’t supposed to turn out this way for the U.S. equity market. Apart from ongoing concerns about excessive valuations, we had an inversion of the yield curve, an earnings recession, Trump’s trade and tariff wars, and the ongoing presidential impeachment process.

Against this backdrop of negatives, the S&P 500 has had a year-to-date total return of 27.6% as of the end of November. For perspective, that’s nearly three times the index’s average annual return of 9.8% over the last 50 years.

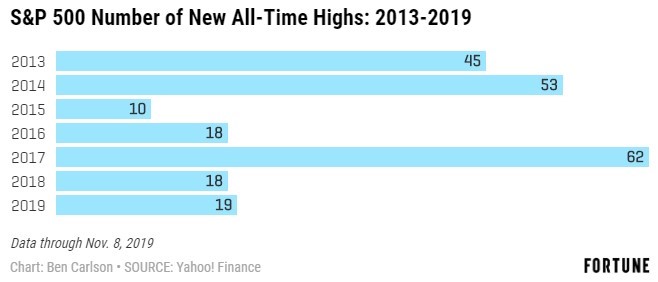

During the current bull market, which has now stretched to 10.7 years, the S&P 500 has set 233 all-time closing highs, with the first new post-financial-crisis peak occurring in 2013. The following chart breaks down the all-time closing highs through Nov. 8—and there have been more since then.

TINA: There Is No Alternative (to Equities)

How to reconcile the stunning returns of stocks in 2019 with all the supposed bad news for the markets? Quite simply: TINA, or “There Is No Alternative”—to equities, that is. Let’s begin with a few equity valuation basics to set the stage.

- On Nov. 29, 2019, the S&P 500 closed at 3,140.98.

- As of Nov. 29, the consensus 12-month forward earnings estimate for the S&P 500 is about $177.

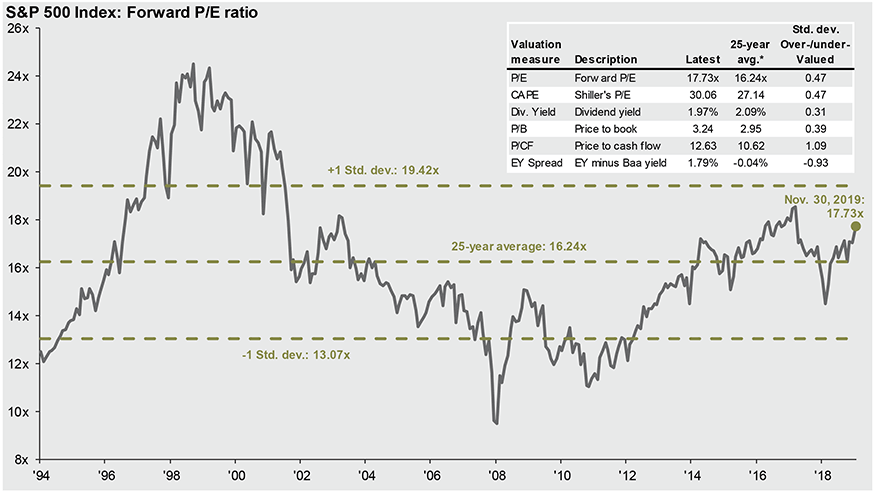

- Based on this estimate, the forward 12-month P/E ratio for the S&P 500 is 17.7x, and the corresponding earnings yield (the inverse of the forward P/E) is 5.6%.

- The following chart from J.P. Morgan Asset Management illustrates that the current forward P/E multiple is about a half of a standard deviation above the 25-year average of 16.2x.

If we restrict our asset allocation universe to the traditional marketable securities of stocks, bonds and cash, the situation begins to make some sense. Let’s consider some pairwise comparisons using data and prices as of the end of November 2019.

- 3-month Treasury bills (1.6%) vs. inflation (1.8%, October CPI): Advantage inflation.

- 10-year Treasurys (1.8%) vs. inflation (1.8%): Advantage even (0% real return).

- S&P 500 dividend yield (2.0%) vs. 10-year Treasurys (1.8%): Advantage S&P 500 dividend yield.

- S&P 500 earnings yield (5.6%) vs. Moody’s Baa bond yield (4.0%): Advantage S&P 500 earnings yield.

The last comparison is really the clincher. Although equities are overvalued by nearly all conventional metrics relative to 25-year averages, depending on geography, we’re either in a low, zero, or negative interest rate environment. (According to recent data from Bloomberg, the global stock of negative yielding debt is now in excess of $17 trillion, representing 30% of all investment-grade bonds.)

To simplify: The S&P 500 earnings yield of 5.6% is 1.6 percentage points higher than the roughly 4% yield available from investment-grade bonds. By this metric, stocks are actually undervalued relative to competing debt.

To complete the hypothetical return picture for large-cap equities, add in a dividend yield of 2%, for a total of 7.6%. With the Fed’s target inflation rate of 2%, the inflation-adjusted or real yield comparison is 5.6% for equities versus 2% for investment-grade bonds—a differential of 2.8x, slightly above the historical average of about 2.3x.

It is true that relative to any single metric, most measures of equity valuations today are higher than their historical averages. But this is a one-factor analysis in a two-factor equation. There is a crucial variable missing: interest rates.

Finance 101 taught us that equity prices are determined by the present value of future dividends. And capital always has a choice among different asset classes. Valuations, therefore, are dependent on interest rates. All else being equal, higher interest rates mean lower valuations and vice versa.

No one, let alone Wall Street forecasters, can ever predict—or explain after the fact—short-term movements in the market. However, historical data tells us that the total return of stocks over the last century has averaged about 10% per year. Stocks could just as easily have been down 25% in 2019—or in any given year.

But unless and until there is an increase in either interest rates and/or credit spreads, the 2% real, inflation-adjusted return from bonds remains unattractive relative to equities. In this historically ultra-low interest rate environment, there is no alternative to equities for building and maintaining wealth.

Behavioral Takeaway

Narrow framing involves making decisions without considering all the implications. In a financial context, it means evaluating too few factors regarding an investment. Regardless of the methodology used for valuing equities, there is always some measure or stream of cash flows—such as dividends or earnings—that must be discounted by some interest rate. In its simplest form, it’s a two-factor model. Valuing equities solely relative to a historical average crucially ignores the variable of interest rates. Such one-dimensional, narrowly framed thinking has caused many investors to make costly errors by shunning equities.