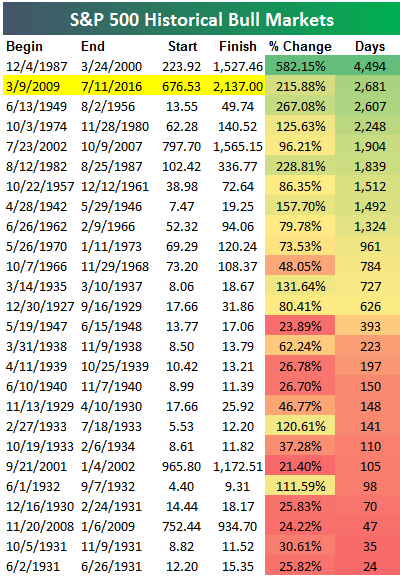

The Second Longest Bull Market Ever…and Counting

What if you threw a party but nobody came? That’s the way the stock market must be feeling these days.

With the S&P 500’s closing high on July 11, the current bull market that began on March 9, 2009, officially became the second longest on record at 2,681 days (7.3 years), surpassing the previous No. 2 that ended nearly 60 years ago (Aug. 2, 1956).

But there’s still a long way to go to eclipse the all-time record of 4,494 days (12.3 years) that ran from Dec. 4, 1987, to March 24, 2000. To get there, the bull market would need to make it past June 28, 2021, without experiencing a decline of 20% or more from a closing high.

The chart below helps put the current bull market in historical perspective, both in terms of duration and percentage change. As to the latter metric, this bull only ranks No. 4 (with a 216% increase as of the chart date of July 11).

(Source: Bespoke Investment Group)

Perhaps because this bull market is not yet a “winner” in the eyes of many—pundits especially—it remains suspect. But there is no denying that the investing public is missing the party.

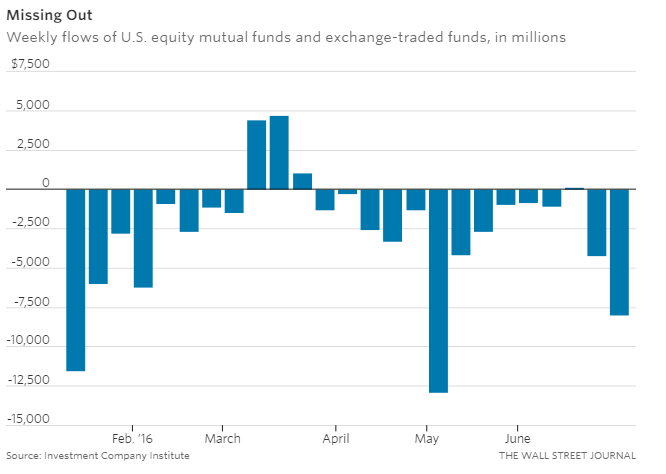

Consider this sobering data from Morningstar: From January through May 2016, investors liquidated an estimated net $52 billion from U.S. equity mutual funds and exchange-traded funds. And that was before the Brexit vote on June 23, 2016.

According to data from the Investment Company Institute (ICI), investors pulled nearly $8 billion from U.S. equity funds in the week post-Brexit. It’s been the same story all year.

And where is all that money going? ETFs that invest in emerging market bonds and junk bonds. Stay tuned for how that will work out.

And 2016 is no anomaly. According to ICI, the outflow from domestic equity funds was $25 billion in December 2015 and $171 billion for all of 2015 (a year with an S&P price return of -0.7%, and a total return of 1.4%).

The Cost of Missing the Party

We constantly pound the drums about the folly of market timing. Trying to gain advantage by getting in and out of the stock market is a fool’s errand, if there ever was one.

We’re spoiled because we have so many ways to demonstrate this numerically. So in the spirit of non-discrimination, we’ll rotate the evidence. The object of our focus today will be the cost of being out of the market. And since we’re in 2016, we’ll focus on the number 6 in an effort to make this illustration more memorable.

Over the last 6 years (July 23, 2010, to July 22, 2016):

- The S&P 500 was up an average of 14.6% year on a total return basis (i.e., with dividends reinvested).

- If you missed the 6 best days in total during this period (i.e., not the 6 best days of each year), the average annual return drops to 10.1%—a reduction of 31%.

- If, out of the 1,511 trading days in this 6-year period, you missed the best 1% of all days (or 15 days in total), the average annual return drops to 5.6%—a reduction of 62%.

(Source: By the Numbers, July 25, 2016)

Again, some historical perspective is required to put all of these numbers in proper context. Since 1926, large cap stocks have generated a total return of about 10% per year on average.

Since the bear market bottom on March 9, 2009, the S&P 500 has increased from about 676 to 2,175 (as of July 22, 2016)—an increase of 221% in price only (and excluding dividends).

Had you been in the stock market—and remained fully invested at all times—since the last bear market bottom—you would have enjoyed an annual total return over these last 6 years almost 50% above average (14.6% compared with 10%). As always, past performance is no guarantee of future results.

But you have to be in it to win it. Sadly, too many investors who desperately need the returns to fund ever-increasing retirement periods have missed the party.

Key Behavioral Takeaway: Narrow Framing

Behavioral biases can be categorized in many ways, and many of these categories may be overlapping or indistinguishable. So we will highlight only one behavior to make the point.

Narrow framing involves the evaluation of too few factors that may affect an investment, or making decisions without considering all the implications.

Investors are afraid and are pulling back. They don’t know what to do with their money as they wrestle with historically low interest rates, the uncertainty surrounding the next presidential election, and the disintegration of world order, among other worries.

So even though cash has provided no return and though the stock market is enjoying its second-longest bull market ever, investors keep selling stocks and refuse to join the party. A multi-decade (or even transgenerational) investor needs to think in terms of longer time horizons, and then sit back and enjoy the ride.