Responding to Rising Rates

In his Feb. 27, 2021, letter to Berkshire Hathaway shareholders, Warren Buffett pointedly warned about the unattractiveness of bonds in the current market environment:

And bonds are not the place to be these days. Can you believe that the income recently available from a 10-year U.S. Treasury bond—the yield was 0.93% at yearend—had fallen 94% from the 15.8% yield available in September 1981? In certain large and important countries, such as Germany and Japan, investors earn a negative return on trillions of dollars of sovereign debt. Fixed-income investors worldwide—whether pension funds, insurance companies or retirees—face a bleak future.

In February alone, the 10-year Treasury rose 0.37 percentage points (from 1.09% to 1.46%). That’s the largest rise in the 10-year note yield since November 2016, when the yield went from 1.84% to 2.37%—a jump of 0.53 percentage points.

The sharp increase in bond yields in February, which largely reflected investor expectations of a strong economic recovery, has caused jitters in the stock market and is forcing investors to seriously confront the implications of rising interest rates.

Bond price sensitivity to rising interest rates

Bond prices are inversely related to yields, and the duration of a bond is a measure of when investors get their money back. Longer-term bonds have higher durations—as do bonds with lower coupon payments, because low coupons mean more waiting. A rule of thumb is that a one percentage point change in interest rates implies a change in the bond’s price equal to the duration.

As of March 5, the most recently auctioned 10-year Treasury due February 15, 2031, had a coupon of 1.125% and a yield to maturity of 1.57%, with a duration of about 8.3. So an increase in the 10-year yield to 2.57% would cause the bond price to decline by 8.3%.

Retirees relying on annual withdrawals from portfolios heavily weighted toward bonds are particularly exposed to this serious risk.

Stocks have countervailing forces at work; net effect is unclear

Expectations of a stronger economy count as a positive development for companies’ earnings prospects, but they are also pushing long-term interest rates higher. While bond prices have an inverse relationship to yields, changes in stock prices fluctuate in response both to expected future cash flows to investors and the discount rate on those cash flows (i.e., it’s a two-variable equation).

All else being equal, the expected cash flows of companies are considered less valuable when yields are higher. But since the increase in the discount rate may be partially or totally offset by an increase in earnings, the ultimate impact on stock prices in a rising rate environment is indeterminate.

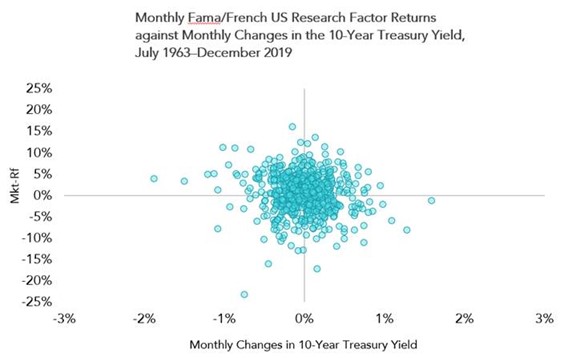

Proving the point, Dimensional Fund Advisors recently examined the correlation between monthly changes in interest rates and stock returns. Consider the range of monthly stock returns in both rising and declining 10-year Treasury yield environments:

- Rising yields: -17% to 15%

- Falling yields: -24% to 16%

Conclusion: There is no clear pattern between yield changes and subsequent stock returns.

Responding to potential future rate increases

How should an individual investor respond to a possible future increase in interest rates? This is a bit of a trick question, because the correct answer is a function of one’s current asset allocation and the methodology used to generate it.

If you’re saving for retirement and other cherished goals, you should have a written, date- and dollar-specific financial plan. By embracing the mindset that your portfolio is the medium to fund your plan, your portfolio construction should be informed by this rational, easy-to-understand asset allocation methodology:

- Cash: One or two years’ worth of living expenses (depending on age and work situation)

- Bonds: A sum sufficient to cover all foreseeable capital needs for the next five years

- Stocks: All remaining funds

Assuming you have a solid financial plan and portfolio in place, there is nothing left to do except patiently let the plan work, so your portfolio can grow over time. And if your plan hasn’t changed, there is absolutely no need to change your portfolio, aside from minor periodic rebalancing.

If you don’t have such a plan in place, the worst thing you could do is make tactical changes in an attempt to time the market. The results would likely not be good—and could be disastrous, potentially ruining your ability to achieve your lifetime financial goals. It’s best to first create a plan and then construct a portfolio using a sound approach to asset allocation.

In short, if you adopt our simple asset allocation methodology, there is nothing to do and no need to respond to a potential future increase in rates.

Behavioral Takeaway

When it comes to achieving your lifetime financial goals, there are only three determinants that truly matter: financial planning, asset allocation and behavior. If you get the first two right, the final—and often greatest—challenge is exercising faith, patience and discipline over time.