Responding to a Recession

“The first rule of compounding: Never interrupt it unnecessarily.” —Charlie Munger

What tactical changes should you make to your portfolio in response to the prospect of a recession? None.

Recession basics

According to the National Bureau of Economic Research, which is responsible for pinpointing the start and end dates of recessions, there have been eight recessions in the United States since 1970. The NBER considers a variety of economic factors, such as retail sales, industrial production, nonfarm payrolls and gross domestic product, to make its determinations.

The most recent recession was the Covid-19 episode of 2020. At three months, it was the shortest recession of the last century but also the most severe in terms of economic contraction, with a decline in GDP of 19.2%. This incident was an extreme outlier caused by the government-induced shutdown of large swaths of the economy. For perspective, the next most severe recession of the eight was the Global Financial Crisis contraction of 5.1%, which started in late 2007.

As of October 2022, we may or may not already be in the next recession. It’s unknowable until after the fact, when the NBER has crunched all the numbers and made its determination.

Meanwhile, in a bit of a better-late-than-never approach, Jerome Powell and the Federal Reserve have been raising interest rates sharply in an effort to kill the cancer of inflation. By making borrowing more expensive, and thus slowing the economy, the result could be the proverbial “hard landing” of a recession.

The Federal Reserve Board employs more than 400 Ph.D. economists[1]. Alas, neither this brain trust, nor anyone else, can reliably or consistently predict the economy. Too many variables are at play. Thus, whether or not we are in or will enter a recession, now or at any time in the future, is also unknowable.

Recession data

Despite the peculiar impossibility of pinpointing recession start dates in real time, we are nonetheless able to compile and analyze historical data to understand the implications for equity investors.

Let’s look at the key data for the last eight recessions, which took place over the last half century or so. The following tables summarize this data.

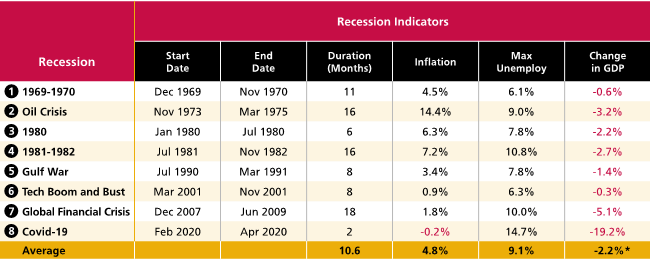

Recession indicators

In this sample, the average duration was just under 11 months, the average inflation rate was 4.8%, the average maximum unemployment rate was 9.1%, and the average change in GDP was -4.8%. Excluding the Covid outlier, the average GDP contraction was 2.2%.

Furthermore, from December 1969 through December 2021, the U.S. economy was in recession 85 out of 636 months — a little over 13% of the time. During the same period, the S&P 500 increased from 92 to 4,766—or nearly 52x (excluding dividends). In other words, the temporary declines associated with these relatively brief recessions were meaningless in the context of an astounding long-term uptrend in equity prices.

Stock market downturns

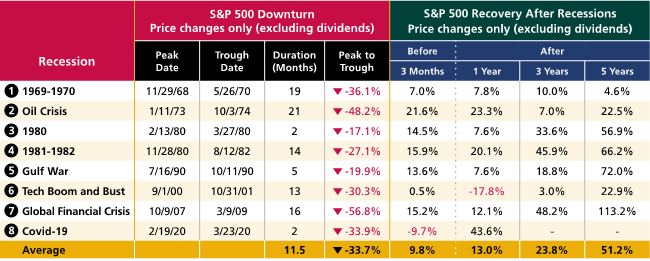

Using the S&P 500 as the benchmark, the market peak-to-trough had an average duration of 11.5 months, and the average peak-to-trough decline was just under 34% (price only, excluding dividends).

*Excluding the Covid-19 recession

Stock market recovery following recessions

The most illuminating data are in the far-right section of the second table. Following a recession, on average, the S&P 500 price (excluding dividends) was up 13.0% after 1 year, 23.8% after 3 years, and 51.2% after 5 years.

What’s far more interesting are the S&P 500 returns 3 months before the recession end dates, which on average were 9.8% (excluding dividends). In our graphical visualizations of the last eight recessions, you can see that in all cases but the Tech Boom and Bust of 2001 (an 8-month recession), the stock market bottomed before the recession’s end.

What does this mean for us as long-term equity investors?

All these data points go to prove the point that just as the economy can’t be predicted, markets cannot be timed. This is one of the iron laws of successful long-term investing. There is simply no way of knowing when a recession is coming, how long it will last, or how intense it will be. Therefore, there is no way to make sound decisions on when and what to buy and sell based on a recession.

Legendary investor Sir John Templeton famously observed, “Among the four most dangerous words in investing are: ‘It’s different this time.’” Any recession-related correction or bear market is an opportunity for the accumulator, a relative nonevent to the fully invested, and a blip in the investing careers of everyone. This time will not be different.

If your financial plan hasn’t changed, don’t change your portfolio. In short, there is nothing to do and no need to respond in anticipation of a recession—now or ever. Instead, be guided by Charlie Munger’s first rule of compounding: Never interrupt it unnecessarily.

Behavioral takeaway

When it comes to achieving your lifetime financial goals, there are only three determinants that truly matter: financial planning, asset allocation and behavior. If you get the first two right, the final—and often greatest—challenge is exercising faith, patience and discipline over time.

[1] Economists, Board of Governors of the Federal Reserve System website.